Table of Contents

Electronic monitoring market set to reach US.2bn by 2030 as EM programmes expand across Europe, the Americas and Oceania

Berg Insight, the leading IoT market research provider, today released new findings about the market for Electronic Monitoring (EM) of offenders.

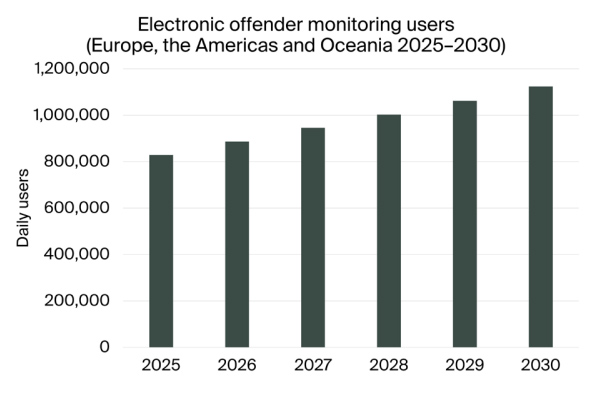

The number of simultaneous participants in EM programmes in Europe, North America, Latin America and Oceania amounted to about 92,000, 564,000, 162,000 and 11,000 respectively during 2025.

The total number of EM programme participants during the full year 2025 reached 285,000 in Europe, 959,000 in North America, 357,000 in Latin America and 33,000 in Oceania.

Berg Insight estimates that the number of simultaneous participants will grow to 130,000 in Europe, 700,000 in North America, 278,000 in Latin America and 16,000 in Oceania by 2030. The market value in 2025 reached US$ 365 million in Europe, US$ 1.1 billion in North America, US$ 97 million in Latin America and US$ 31 million in Oceania. The total market value in the four regions combined is forecasted to grow at a CAGR of 5.9 percent from US$ 1.6 billion in 2025 to US$ 2.2 billion in 2030.

Electronic monitoring (EM) programmes was first introduced in the US in the early 1980s. Today, EM is an established alternative to detention across Europe and North America and in some Latin American and Oceanian countries. EM programmes aim to increase offender accountability, reduce recidivism rates and enhance public safety by providing an additional tool to traditional methods of community supervision. Policy makers, corrections authorities and private sector service providers advocate for extended EM programmes to reduce total correctional system costs and to combat prison overcrowding.

There are two dominant technologies used for electronic monitoring – Radio Frequency (RF) and GPS. RF-based systems are today the most common type of solution in most European countries. In the US, Australia and New Zealand in Oceania, Brazil and other countries in Latin America, GPS-based solutions are used in the vast majority of cases. A number of private companies are involved in the provisioning of EM, including developing, supplying and installing equipment, providing monitoring services as well as delivering other supporting services.

Leading providers of EM equipment and services include US-based BI Inc. (GEO Group), Allied Universal Electronic Monitoring, Sentinel Offender Services, SCRAM Systems, Securus Technologies, Shadowtrack, Corrisoft, Talitrix and Track Group; UK-based Buddi; Israel-based SuperCom; China-based Refine (REFINE Technologies); Switzerland-based Geosatis; and Brazil-based Spacecom, Synergye and UE Brasil Tecnologia.

Even though electronic monitoring has been around for about 40 years, the form factor of the monitoring device has changed little. New discreetly designed wrist-worn GPS devices have emerged in recent years, making monitoring less intrusive for wearers and reducing the stigma associated with ankle bracelets. Devices that combine GPS tracking and alcohol monitoring are also increasingly used as part of EM programmes.

“Solutions aimed to protect the victims of domestic violence and other violent crimes from the offender have been growing in use in the past few years”, continues Mr. Andersson.

Some countries have expanded the use of domestic violence programmes as these offences have become more common in some jurisdictions. Public concern has further intensified pressure on governments to respond to the growing number of offences related to domestic violence. At the same time, prison overcrowding and rising incarceration costs continue to impose major challenges for many jurisdictions.

What Technology Advances Are Reshaping the Ankle Monitor Industry?

Three shifts define the GPS ankle monitor market transition: adaptive multi-mode connectivity (BLE/WiFi/LTE extending battery from days to months), fiber-optic tamper detection (eliminating 15-30% false-alarm rates), and AI-driven alert management reducing officer fatigue by 60-80%.

The GPS ankle bracelet market is moving from Generation 3 (cellular-only, 24-72h battery) to Generation 4 (multi-mode connectivity, 7-180 day battery, zero false-alarm tamper detection). This addresses three scaling barriers: daily charging consuming officer time, cellular dead zones creating gaps, and false alerts preventing effective caseload management.

For agencies evaluating electronic monitoring investments, the vendor’s technology roadmap matters as much as current specs. 5G compatibility (LTE-M/NB-IoT), smartphone integration, and cybersecurity certification (EN 18031) will define competitive positioning through 2030. Programs locked into legacy ankle monitor equipment face forced replacement as 3G shutdowns continue globally.

How Do International Programs Inform Global Electronic Monitoring Best Practices?

Electronic monitoring programs across 30+ countries provide diverse implementation models that inform technology requirements, supervision standards, and policy frameworks — creating a knowledge base that benefits procurement teams evaluating GPS ankle monitor systems for any jurisdiction.

The variation in international approaches reveals how different legal frameworks shape GPS ankle bracelet technology requirements. European programs operating under GDPR mandate strict data minimization and purpose limitation controls built into monitoring platforms. Asian programs — particularly South Korea’s comprehensive sex offender tracking system — demonstrate the technical requirements for lifetime monitoring with victim-facing notification capabilities. Latin American deployments show how electronic monitoring can scale rapidly as an alternative to chronically overcrowded prison systems.

For GPS ankle monitor manufacturers, this global diversity drives technology innovation: devices must support multiple cellular standards (LTE-M/NB-IoT across different carrier ecosystems), multilingual monitoring platforms, configurable data retention policies, and varying levels of enrollee-facing features. Vendors with proven deployments across 30+ countries demonstrate the manufacturing maturity, supply chain reliability, and technical adaptability that single-market providers cannot match.

The international electronic monitoring landscape consistently validates three technology priorities regardless of jurisdiction: extended battery life reduces operational burden, reliable tamper detection maintains program credibility, and multi-mode connectivity ensures supervision continuity across diverse geographic and infrastructure conditions.